30-yr fixed (PMMS, Jun 4)

6.48%

15-yr fixed (PMMS, Jun 4)

5.79%

30-yr fixed APR (Bankrate, Jun 10)

6.62%

52-week low (30-yr)

6.09%

One year ago (30-yr)

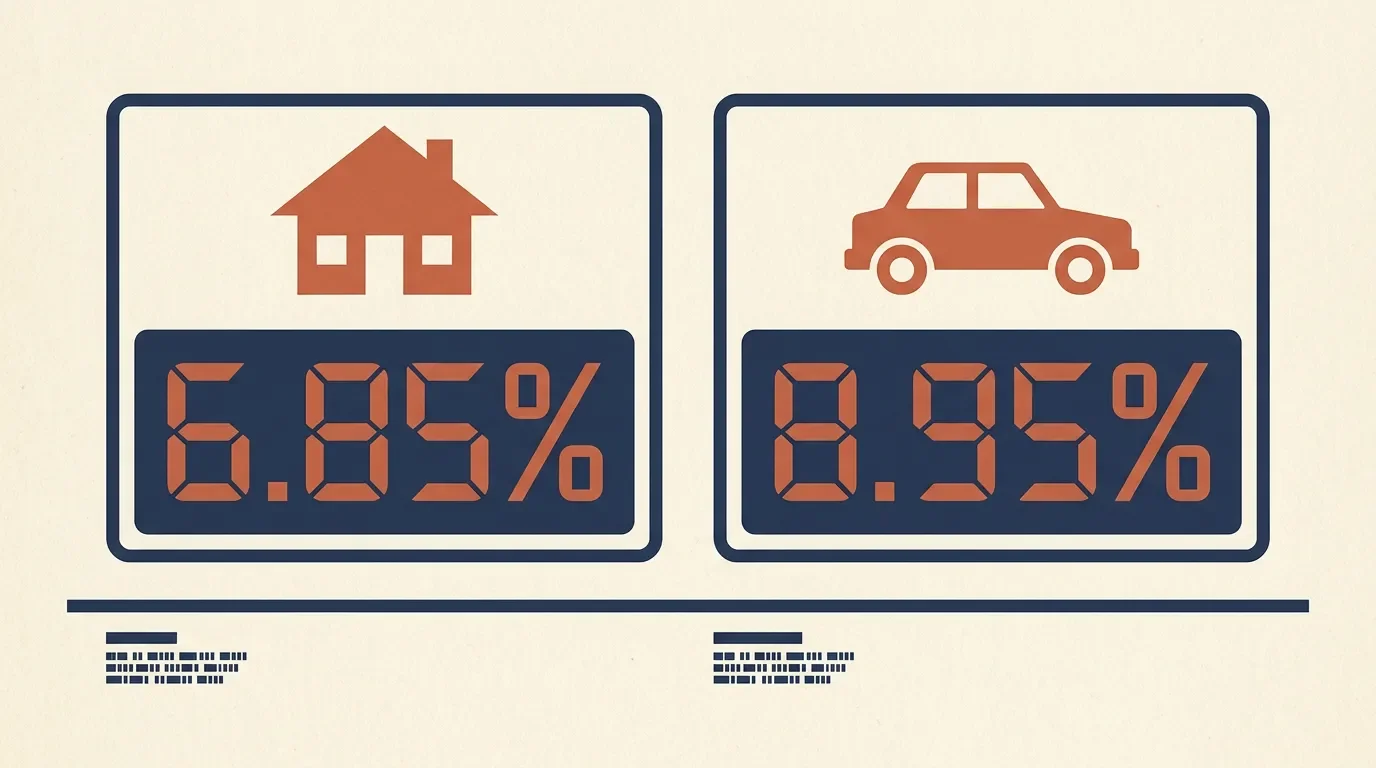

6.85%

Freddie Mac's June 4 survey puts the 30-year fixed at 6.48%, a modest dip from 6.53% but still well above historical norms. Auto loan rates top 6.9% for new 60-month financing. This issue breaks down the current numbers on both markets, explains why the Fed is unlikely to cut rates soon, and offers a clear-eyed framework for anyone weighing a purchase decision this summer.

Financial disclaimer: This article is for informational purposes only and does not constitute financial, investment, or lending advice. Rates change daily. Consult a qualified financial advisor or lender before making any borrowing or purchasing decision.

| Loan type | Interest rate | APR |

|---|---|---|

| 30-year fixed | 6.55% | 6.62% |

| 15-year fixed | 5.93% | 6.03% |

| 30-year FHA | 6.45% | 6.49% |

| 30-year VA | 6.52% | 6.57% |

| 30-year jumbo | 6.71% | 6.75% |

| 5/1 ARM | 5.72% | — |

| Loan term | Average rate |

|---|---|

| 48-month new car | 6.75% |

| 60-month new car | 6.92% |

| 36-month used car | 7.24% |

| 48-month used car | 7.41% |

| Credit band | New car APR | Used car APR |

|---|---|---|

| 781–850 (super prime) | 4.66% | 7.70% |

| 661–780 (prime) | 6.27% | 9.98% |

| 601–660 (near prime) | 9.57% | 14.49% |

| 501–600 (subprime) | 13.17% | 19.42% |

| 300–500 (deep subprime) | 16.01% | 21.85% |

Disclaimer: Rates quoted are national averages from third-party surveys (Freddie Mac PMMS, Bankrate) and do not represent an offer to lend. Your actual rate will depend on your credit profile, loan-to-value ratio, lender, and market conditions at time of application. This content is informational only and is not financial, legal, or lending advice.

Add more perspectives or context around this Post.